Table Of Content

Following the COVID-19 pandemic, the Fed implemented an expansionary monetary policy to help the economy, resulting in great rates for homeowners. If a homeowner has not taken advantage of the great rates in the last two years, they should refinance as soon as possible to try to lock in a lower rate. In fact, due to the increase in inflation, the Fed has signaled that it will increase short-term rates and reduce the QE programs, resulting in higher rates for refinancing. If you want to uncover more about the best mortgage lenders for low rates and fees, our experts have created a shortlist of the top mortgage companies. Some of our experts have even used these lenders themselves to cut their costs. For example, you might find that a lender offers different rates for conventional loans and government-backed loans.

How to buy down your mortgage interest rate - CNBC

How to buy down your mortgage interest rate.

Posted: Wed, 17 Apr 2024 07:00:00 GMT [source]

How does a 30-year fixed-rate mortgage compare to an ARM?

I’ve twice won gold awards from the National Association of Real Estate Editors, and since 2017 I’ve served on the nonprofit’s board of directors. Bankrate scores are objectively determined by our editorial team. Our scoring formula weighs several factors consumers should consider when choosing financial products and services. If you're buying when rates are high, you'll need to adjust your homebuying plans accordingly.

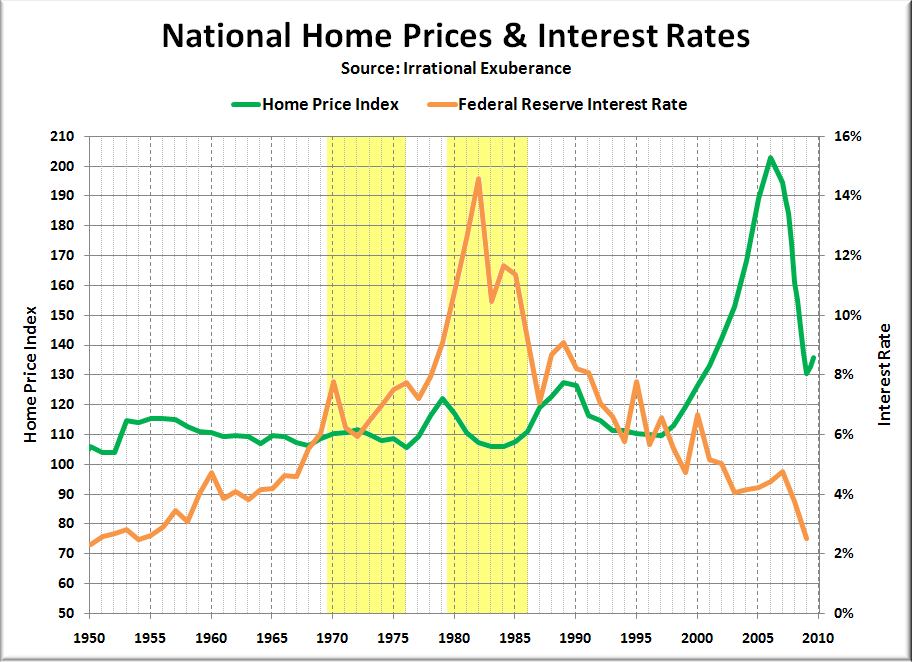

Homeowners May Want to Refinance While Rates Are Low

Projected Interest Rates in 5 Years: A Look at the Forecasts - Norada Real Estate Investments

Projected Interest Rates in 5 Years: A Look at the Forecasts.

Posted: Wed, 24 Apr 2024 07:00:00 GMT [source]

Many homeowners have taken the opportunity to refinance in this low rate environment, and it isn't too late to do so. For whatever reason, borrowers sometimes choose not to refinance when it is in their best interest to do so. So, homeowners should definitely take the time to compare their existing mortgage rate and see if they can do better. The Federal Reserve has been working to bring inflation to a more sustainable level of 2 percent.

How does the Federal Reserve affect mortgage rates?

In today’s hot market, sellers often accept cash transactions ensuring that the deal will close, which can be a risky choice for the buyer. The danger to the buyer is that they may be overpaying for the home. With no appraisal needed for a loan, there is no independent third party providing an estimate for the value of the home. Ultimately, if homebuyers are looking to get the best price on a home, they should exercise caution if paying for a home with cash, or instead take advantage of historically low mortgage rates. When interest rates are higher, you have to make bigger monthly payments compared to the payments for the same loan at a lower rate.

How do I get the best mortgage rate?

From March 2022 to July 2023, the Fed raised its policy rate 11 times, leading to a surge in mortgage rates. A change in demand for 10-year Treasury bonds and mortgage-backed securities also contributed to 2023’s higher rates. If you know how much you’re borrowing, what type of loan you’re getting and how many years you have to pay it back, you can use a mortgage calculator to check your monthly payment at different interest rates. The average homeowner is now forking out a record $2,800 just to cover their monthly payment, as soaring house prices and surging interest rates have made it costlier than ever to own a home.

How can I refinance my 30-year mortgage?

The budget deficit remains high, and the various inflation metrics remain above the comfort level. That means the mortgage rates will likely be in the 6% to 7% range for most of the year. As we head into the spring home buying season, the 2024 outlook for mortgage rates is mainly optimistic, although most experts expect only a small decline.

How to Negotiate Mortgage Rates

And, if lenders know you’re shopping around, they may even be more willing to waive certain fees or offer better terms for some buyers. They all use different formulas to determine a borrower’s ‘risk’ and set rates accordingly. Lenders may also adjust rates depending on their current workload and desire for new loans. That can vary from day to day and from one borrower to the next.To find the lender with the best rates for you, shop around. Compare rates and fees from at least 3-5 lenders, and choose the one with the lowest overall cost for you. It’s important to look at annual percentage rate (APR) as well as current mortgage rates.

How We Make Money

Mortgage rates are always changing, and there are a lot of factors that can sway your interest rate. Some of them are personal factors you have control over and some aren't. The lender will gather these details when you apply for a mortgage preapproval and will provide an estimate of a personalized rate.

While we adhere to strict editorial integrity, this post may contain references to products from our partners. This table does not include all companies or all available products. The better your credit score, the better the rate you'll get on your mortgage. To access the best mortgage interest rates, aim to have a credit score at least in the 700s. As with other types of mortgages, you'll want to shop around and get multiple rate quotes to find the best HELOC lenders or home equity loan lenders.

The best mortgage rate for you will depend on your financial situation. The standard 30-year fixed rate mortgage is benchmarked off the 10-year U.S. The spread reflects the "cost" of the mortgage to an investor based on the risks that the borrower could prepay their loan down the road or default on the loan in the future. These costs rise and fall with general economic conditions, including the prevailing interest rate environment causing rates to rise and fall according to changes in the risk of these loans to investors.

The Ascent, a Motley Fool service, does not cover all offers on the market. As The Ascent's Compliance Lead, he makes sure that all the site's information is accurate and up to date, which ensures we always steer readers right and keeps various financial partners happy. The lender should send you a loan estimate with your pre-approval, which is a document that gives you information about the loan you would likely qualify for. Loan estimates all use the same format and make it really easy to compare loans, so if the lender doesn't send it with your pre-approval notification, ask for one. Some lenders charge different interest rates for loans of different sizes. Some charge higher rates on jumbo loans, some charge lower rates for jumbo loans.

No comments:

Post a Comment