Table Of Content

- Mortgage rates and tug-of-war with inflation

- year mortgage rate increases, +0.24%

- What is the mortgage rate forecast for the next five years?

- Mortgage Rates Today: April 22, 2024—15-Year Mortgage Rates Increase, 30-Year Rates Steady

- Cons of a 30-year mortgage

- Factors that affect your mortgage interest rate

- Find Out What You Qualify For

Our mission is to provide readers with accurate and unbiased information, and we have editorial standards in place to ensure that happens. Our editors and reporters thoroughly fact-check editorial content to ensure the information you’re reading is accurate. We maintain a firewall between our advertisers and our editorial team. Our editorial team does not receive direct compensation from our advertisers. While we adhere to stricteditorial integrity,this post may contain references to products from our partners.

Mortgage rates and tug-of-war with inflation

The lowest-risk rate locks are fee free and have a float-down feature. For mortgage pre-approval, the lender reviews your credit history and financial situation and verifies your income. Pre-approvals aren't always a firm commitment to lend, but generally, if nothing in your financial situation or credit history changes, there's a good chance you'll get a green light when you apply.

year mortgage rate increases, +0.24%

The reason is that your rate will be personalized according to your circumstances. Something deeply unusual has happened in the American housing market over the last two years, as mortgage rates have risen to around 7 percent. Homebuilders have been able to mitigate the impact of elevated home loan borrowing costs this year by offering incentives, such as covering the cost to lower the mortgage rate home buyers take on. That’s helped spur sales of newly built single-family homes, which jumped 8.8% in March from a year earlier, according to the Commerce Department. Your estimated annual property tax is based on the home purchase price.

What is the mortgage rate forecast for the next five years?

Kentucky First-Time Home Buyer 2024 Programs and Grants - The Mortgage Reports

Kentucky First-Time Home Buyer 2024 Programs and Grants.

Posted: Tue, 23 Apr 2024 07:00:00 GMT [source]

All mortgage lender inquiries within a certain time period are counted as a single inquiry, whether you apply with one or 999. That's because a creditor that pulls your score might use an older or newer FICO® Score. To protect your credit, make all your applications within a two-week window. At today's average rate, you'll pay $691.02 per month in principal and interest for every $100,000 you borrow. That's an increase of $11.55 over what you would have paid last week.

Importantly, when comparing offers, homebuyers need to take into account other costs beyond principal and interest payments. A smaller down payment doesn't always mean you'll have to settle for a higher rate, though. The interest rates for low down payment loans (like an FHA loan or a VA loan) can be very competitive.

That pushes MBS prices lower and mortgage rates higher.When investors are worried about the economy, they want to buy safer investments to balance the risk in their investment portfolios. That extra demand pushes up the price of MBSs and sends mortgage rates lower. A 30-year, fixed-rate mortgage lets you repay your home loan balance over three decades.

Factors that affect your mortgage interest rate

Current mortgage interest rates: Mortgage rates today - CNN Underscored

Current mortgage interest rates: Mortgage rates today.

Posted: Tue, 19 Mar 2024 07:00:00 GMT [source]

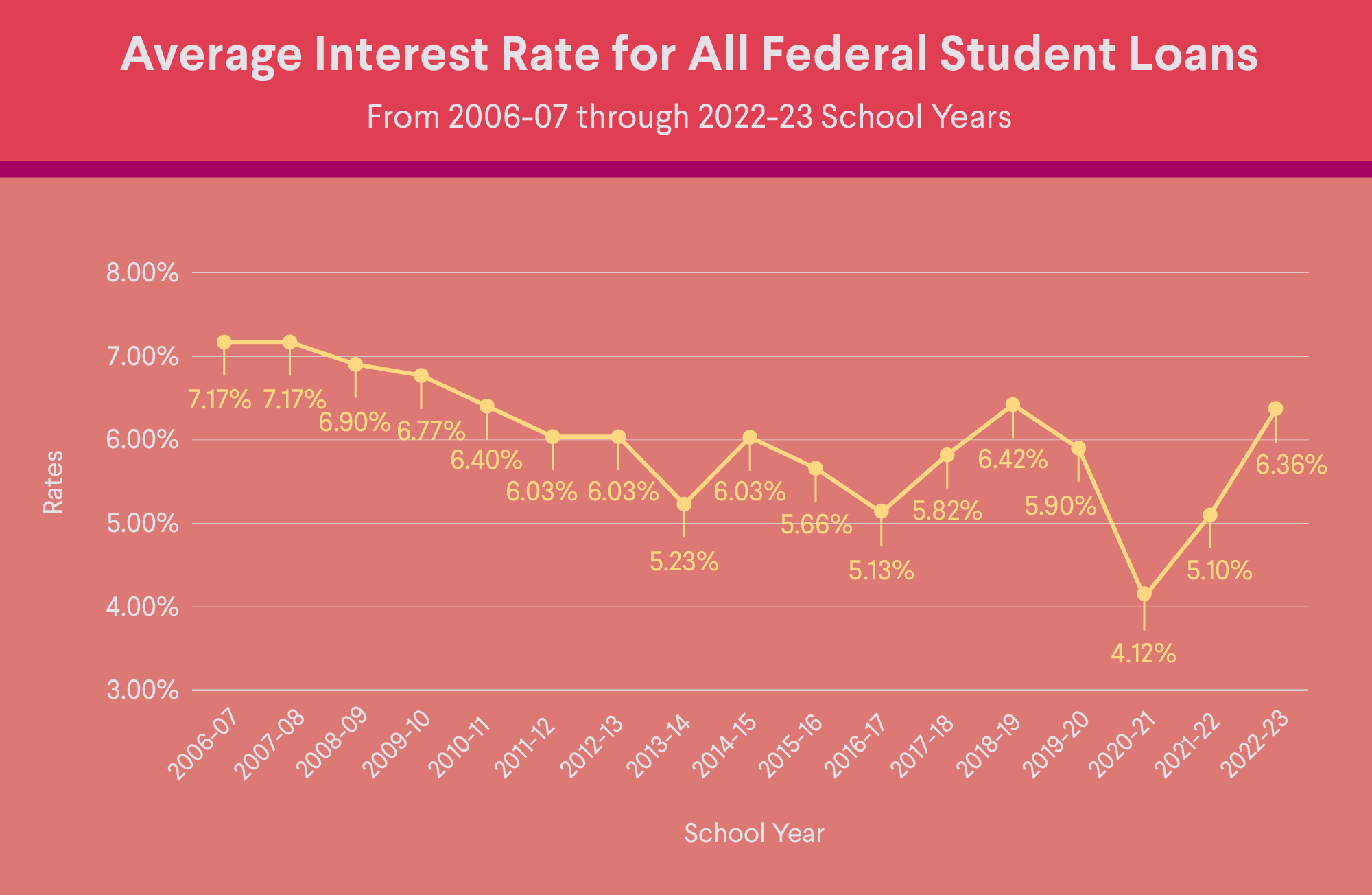

There were also some 14 million mortgage refinances during the same time. If you were lucky enough to secure a mortgage during that time, then 2024 is likely not the ideal time to refinance. Below is a chart of historical montly mortgage rates from the Federal Reserve Economic Data series.

Homeowners need to shop around to look for the best mortgage deal possible. Unfortunately, although the home is the most important asset and the mortgage is the most important liability for most households, research has shown that homebuyers do not do enough shopping. Comparing rates and fees from several lenders is important, not only from traditional lenders such as local banks, but also Fintech lenders.

Top offers on Bankrate vs. the national average interest rate

The further away you are from that happy situation, the higher interest rate you’re likely to pay. A quick way to determine if you should refinance is to estimate your out-of-pocket cost to refinance and divide by your monthly payment savings -- how much your payment goes down due to the refinance. The answer will represent the number of months it will take to get your money back from refinancing, also called the breakeven point. Therefore, if you plan to live in your home longer than the answer to this math problem, you should refinance. If you plan to live for fewer months, then you should not refinance.

States with higher levels of population growth typically see the increased real estate demand drive faster real estate price appreciation. As the COVID-19 healthcare crisis swept the globe governments pushed lockdowns which contracted many economies at record rates. In the second quarter of 2020 the United States economy contracted at a record annualized rate of 31.4%. Writers and editors and produce editorial content with the objective to provide accurate and unbiased information.

Similarly, conventional loans with less than 20% down can have expensive private mortgage insurance (PMI). The stability and predictability that come with fixed rates and low payments are hard to beat. Most home buyers can get a 30-year fixed home loan with a down payment of just 3% or 3.5%. Common mortgage loan types include conventional, FHA, USDA and VA loans. Borrowers with unique needs can also utilize non-qualifying loans that cater to specific financial situations or property types. But once the “teaser” initial rate period expires, your monthly payment could go up based on the terms of the program you chose.

This will put buyers in tight housing situations for the foreseeable future. Mortgage rates are influenced by economic trends and investor demand for mortgage-backed securities. If you're having trouble getting a good rate, you might want to work on improving your credit or saving for a larger down payment and reapply later.

During that time period, your interest rate and monthly payments are fixed — so they always stay the same (unless you refinance). Opting for a 30-year FRM does not mean you need to keep the home all 30 years. You’re generally free to sell the home or refinance into a different loan at any time. A 30-year fixed-rate mortgage is a home loan repaid over 30 years with an interest rate that does not change. The 30-year period is your “loan term,” and usually gives you the lowest monthly payment compared to shorter terms. While average mortgage and refinance rates can give you an idea of where rates are currently at, remember that they're never a guarantee of the rate a lender will offer you.

But you could pay more after that period, depending on how the rate adjusts annually. If you plan to sell or refinance your house within five years, an ARM could be a good option. Since mortgage rates fluctuate for many reasons -- supply, demand, inflation, monetary policy and jobs data -- homebuyers won’t see lower rates overnight, and it’s unlikely they’ll find rates in the 2% range again.

Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information.

No comments:

Post a Comment